Newsletter #17 (2/10/2025)

Honda and Nissan not making it to the altar, water in Texas, and U.S. job growth moderating

There are some absolutely huge construction projects coming this year.

“Wow” is what I said to the reports of several billion dollar projects that were to have broken ground in December (2024), including a $1.6 billion Lyndon B. Johnson Hospital replacement in Houston, $1.2 billion San Antonio International Airport Terminal C development, and a $1.1 billion Hard Rock Hotel in Las Vegas.

Not included in these projects are the proposed nearly $2 billion stadium for the former-Oakland A’s MLB baseball team that could begin construction later this year or the $1.5 billion South Station tower in Boston, which is already underway.

Though Caterpillar notes that construction growth could be muted this year, specifically that the “North American construction segment should see "moderately lower sales to users" that would likely reflect cooler demand for new equipment”, overall 2025 is still shaping up to be a healthy year for construction, albeit at least for projects already close to kickoff. We could see some adjustments to projects being green lit for construction later this year, but for now, it looks like the moderately good times (but not the gravy COVID years) will continue.

That supposed all-but-certain Nissan/Honda marriage didn’t last long.

For all the prognostication that the proposed merger between Nissan and Honda absolutely would happen, I wonder what they are saying now? Looks like this thing is dead in the water after all. Honda just has all the leverage over Nissan here, and Nissan seems to be stuck on negotiating points to the merger they have no business asking for. I wish Nissan all the best here, but I would not blame Honda for walking completely away from this potential deal. It still makes more sense to me for Honda to wait for the Nissan situation to erode further and then attempt a fire sale takeover instead.

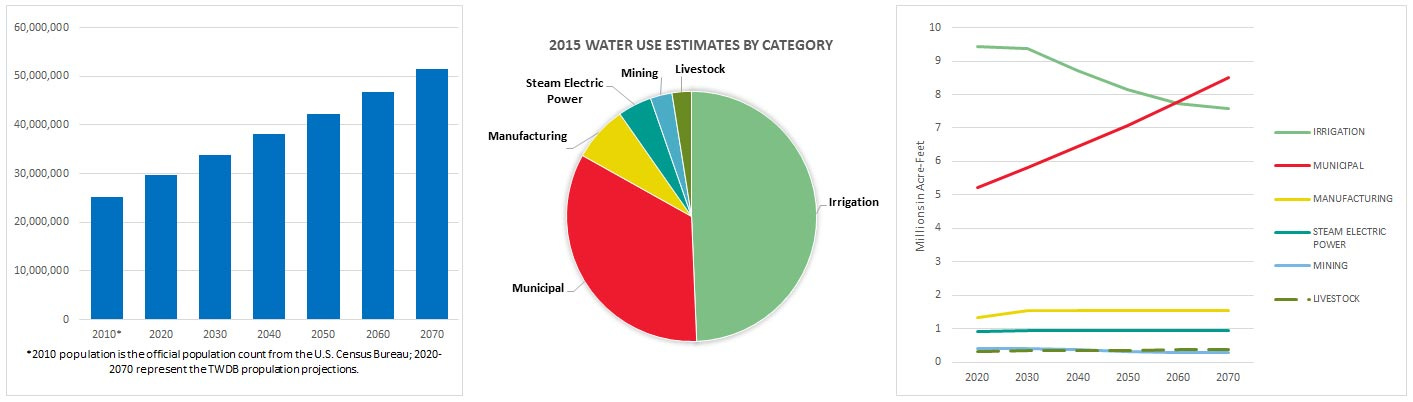

Ignoring the politics of the moment, the State of Texas is finally taking our water needs seriously.

According to a recent announcement by the Governor of Texas, an emergency item for this year’s Legislature has been identified for water investment. While I’ve previously written about the ignorance to this issue by the state government, it is a relief to see the Legislature taking it so seriously now.

According to the information released by the Governor’s office in the announcement, the State is looking to make the largest-ever investment in water infrastructure, including desalinization plans and shipping/piping options, rural water systems and more. More and more, people are becoming more outspoken about this issue due to the population growth of Texas and climate shift the last several years, including farmers and the Water for Texas conference, where the state demographer “stressed the importance of investing in infrastructure as people and businesses move to the state.”

Without this investment, not only will the continued growth of Texas become stagnant, but certain communities could be in real trouble. Here’s hoping the fractured government can recognize a bipartisan issue of significant impact and make it happen. The data shows there is a problem with the state’s water plan, and it must be fixed.

More corporate efficiency announcements are coming.

WorkDay, Billabong, Goodyear, Salesforce, Sonos, Alamo Drafthouse, S&B Engineers, Cruise, Thermo Fisher Scientific are among the latest companies making various announcements to rightsize their organizations for differing reasons, chief among them, though, the repetitively mentioned need for greater corporate efficiency.

Boeing also is in the news again for announcing more layoffs due to their ongoing quality and execution struggles, this time due to their Artemis space program. Texas-based construction behemoth Zachry Holdings is exiting bankruptcy and conducted a series of layoffs to aid their restructuring process. And, finally, Walmart is closing another regional office to further consolidate corporate staff into two primary campuses.

While many companies are still experiencing significant growth and do not seem to be affected by the growing number of cutbacks, I’ll recommend again you should be analyzing your indirect and overhead costs, as well as your staffing plans, for 2025 to determine if you are prepared for an economic slowdown.

So, about that job market…...

The latest Recruitonomics report hit following the latest jobs report for the U.S. labor market, and all is definitely not what it seems. Total employment gains were 143,000 in January 2025, reflecting moderately solid growth but a bit under the roughly 170,000 that was expected. Concerning? Not really, at least on its face.

What does raise eyebrows was the seasonal adjustment that was announced also. In particular, “job growth in the 12 months through March 2024 was revised down by 589,000, so monthly job gains were actually about 50,000 lower per month than initially reported.”

If you combine that with the revision that was announced a few months ago, we can likely reasonably assume a deduction of +/- 50,000 jobs could be made a year from now, from January’s report also, leaving us with around 90,000 actual jobs added in January 2025. Still a significant job growth level for the country and not in the danger zone, but reflects the general moderation we are seeing when you look at the data in chart form like the below.

-------------------------------------------------------------------------------------------------

© February 2025, Brandon Caldwell. All rights reserved. Hyperlinks are used frequently for proper credit to source material on respective websites, news articles, social media or other sources. Images are used with and in credit to rights reserved to their respective owner(s). While it can be a useful tool, no ChatGPT or other generative AI was used in the production of this newsletter. Opinions are mine and do not reflect the opinion or policy of others including employers past or present.